Ebix Inc. (EBIX, Financial) is an Atlanta-based company with operations mainly centered in India. It was started by an Indian immigrant, Robin Raina, who leveraged lower-cost Indian IT talent to put together a data exchange solution for the insurance industry.

The company's most important service is to provide data exchange software-as-a-service solutions for insurance companies, brokers and agents. It also provides back office and risk management services to Insurance companies.

The other major business is Ebix Cash, which provides payment solutions like foreign exchange, remittance and payments as well as travel services. This business is mostly centered in India.

There are a bunch of other businesses like e-learning and travel, but these appear to be minor. The company states that 91% of its revenue comes from its insurance exchange and Ebix cash businesses. The company does not break down its segments further, but it appears the insurance exchange business is the main driver of value. The Ebix Cash business, though, has higher revenue but does not appear to be quite as profitable. Again, it is hard to confirm due to the lack of segment-level transparency.

Ebix is planning to spin off the Ebix Cash business as a separate company on the Indian stock market. It already has separately listed Ebix Cash World Money Ltd. on India's National Stock Exchange. Data from Yahoo India indicates the stock has a market cap of $101.67 million.

The stock is cheap and historical growth is impressive

As can be clearly seen in the chart below, revenue and earnings growth have been impressive. Revenue and earrings per share have grown at over 20% per year over the last 15 years.

Yet the stock only trades at a price-earnings ratio of around 10. This discrepancy is due to a plethora of "red flags."

Auditor resignation

Ebix's auditor, RSM U.S., resigned its engagement in mid-February. RSM told Ebix's audit committee chairman it was resigning as a result of being unable to obtain sufficient evidence to evaluate the business purpose of "significant unusual transactions" in the fourth quarter of 2020, according to a regulatory filing.

The auditor informed Ebix that there was a disagreement with respect to the classification of $30 million and flagged unusual transactions concerning Ebix's gift card business in India. Internal control over financial reporting was not effective as of Dec. 31 due to the identification of a material weakness, RSM said in its resignation letter.

Ebix said it did not agree with certain statements made by RSM and believed that the accounting for its gift card business was consistent with GAAP requirements. The company intends to move as quickly as possible to replace RSM and to complete its 2020 financial audit. (Ebix picked KG Somani to replace RSM. The new firm is a accounting firm based in New Delhi). The 10-K was filed on April 27.

The company has changed auditors many times in the past. Some of the past changes were understandable as the company was expanding internationally and needed to go to auditors with more multinational experience. However, it is worrisome that the company cannot hold on to its auditors. Given the sudden resignation of RSM, the stock fell sharply in March. It has recovered since then, but remains under a cloud. Short interest remains exceedingly high. Yahoo reports that over 20% of the float was short in mid-May. The company is in the crosshairs of dozens of class-action lawyers who are trolling for aggrieved shareholders. The company could end up paying a substantial sum to get itself out of this hole.

Lack of transparency in segment reporting

A big issue I noticed is that in spite of Ebix conducting multiple unrelated businesses, it reports as a single segment. This is odd as it is not clear why it does so. This makes it very hard for investors to analyze and value a business within the corporate umbrella. Everything is lumped together. Since the company continually and aggressively makes tuck-in acquisitions, it becomes very difficult to ascertain if these acquisitions are adding or detracting from the bottom line.

Ebix has spent $812 million between 2008 and 2020 acquiring new businesses. Meanwhile, net income went from around $27 million to $89 million in that period (cumulative income of $946 million in the 2008 to 2020 period). This does not appear to be an impressive return on investment. Return on invested capital has been declining continuously for the last 15 years.

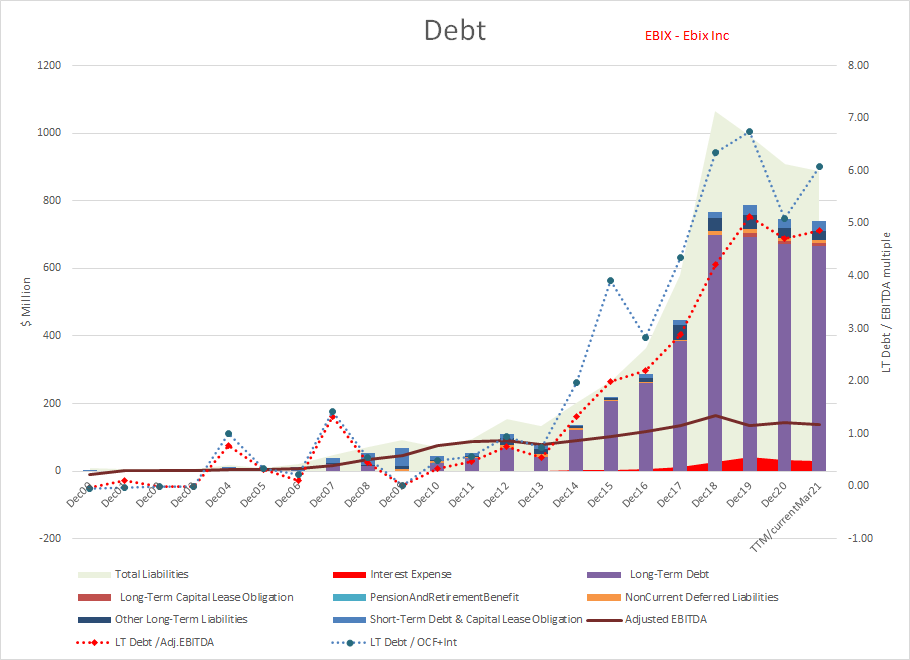

Increasing debt

Another issue of concern is that debt has risen far faster than earnings or cash flow. The company is pursuing top-line growth through acqusitions funded by debt, but the bottom line remains flat.

Conclusion

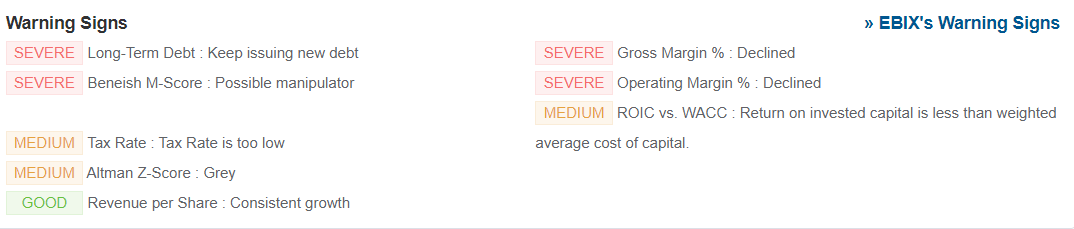

Apart from the red flags outlined above, the GuruFocus system also highlights a number of warning signs, including that it is a potential "value trap" since it is trading far below the intrinsic value.

Ebix is an interesting company that is undeniably cheap and has high top-line growth. It also has a strong presence in the attractive and very large Indian economy. If the company can overcome the reputational challenge of the auditor issue and is able to the execute the Indian IPO of the Ebix Cash business, the stock could easily double.

There are many red flags surrounding this story, however, so it would require a high tolerance for risk to enter this minefield. On the other hand, stocks are rarely this cheap without a lot of "hair" on it. Ebix is a classic "hairy but cheap" stock.

Disclosure: The author does not own stock in Ebix Inc.